Similar to common marine policies and auto policies (make sure to review your specific policy as they can vary), the marine policy typically covers the vessel from the moment it enters the water. Land coverage applies while on roads. The brief transition window — backing down a ramp, entering the water — is generally covered under whichever policy is contextually appropriate. Work with your broker to confirm there are no gaps. In practice, we haven’t seen coverage disputes during transition; the policies complement each other. Consult your broker or policy for guidance or clarification.

We can help with this because the WaterCar EV is considered a US coast-guard compliant recreational vessel complete with a HIN number for the Water. It is also an LSV complete with a VIN number for the road. We can point you toward brokers who have successfully placed WaterCar coverage.

From previous customer’s experiences, Yes. Marine coverage handles watercraft liability, hull damage, and on-water incidents. Land coverage handles road use, collision, and LSV operation. The policies work together without overlap — each covers its environment. Most owners find the combined annual cost reasonable for what they’re insuring.

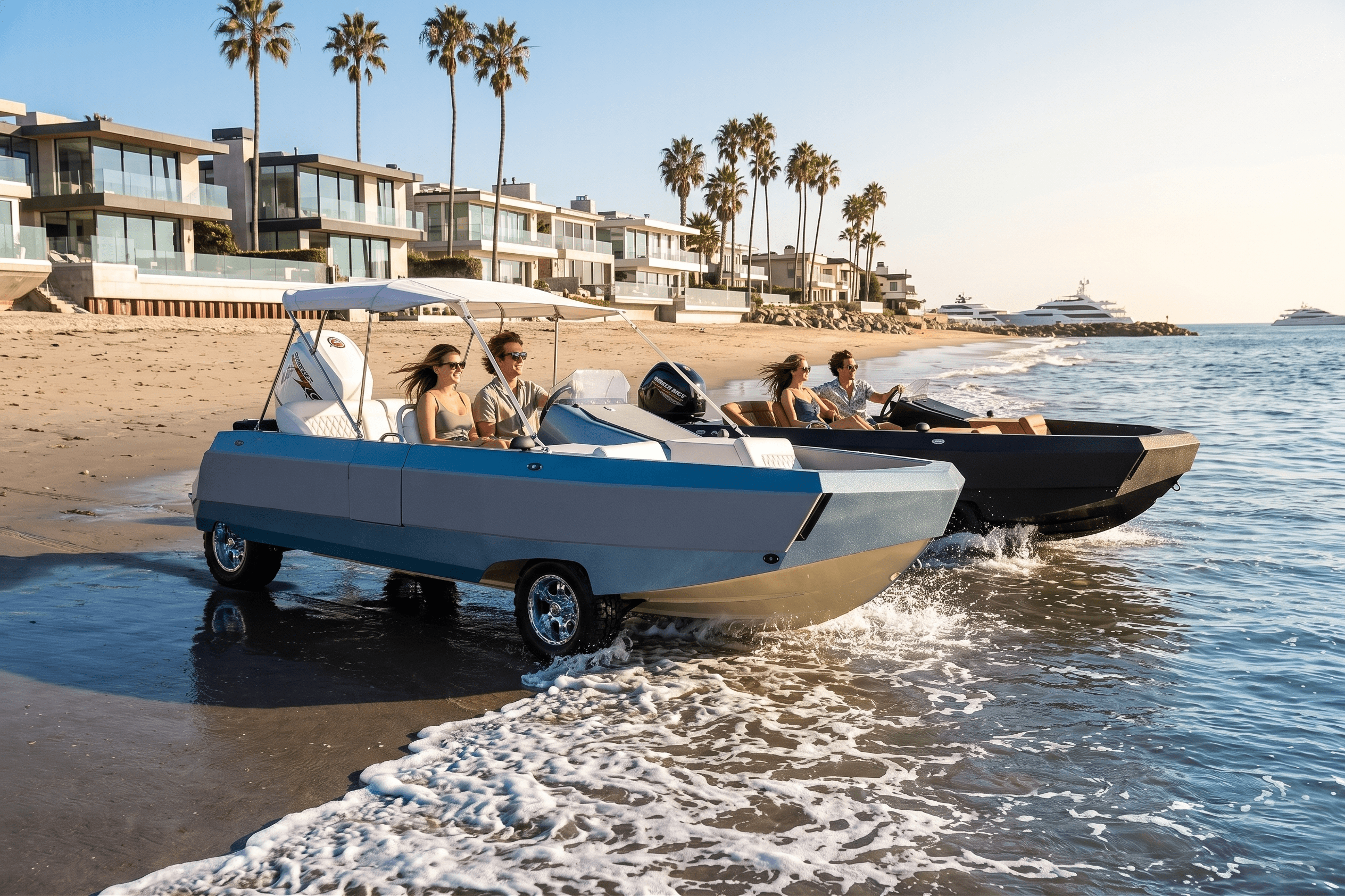

From previous customer experiences, think of it as two separate policies for one vehicle. On the water, it’s an 18-foot recreational pleasure boat with a HIN (Hull Identification Number) — insured through a marine policy as a recreational US coast-guard compliant vessel. On road, it’s a federally certified Low Speed Vehicle with a 17-digit VIN — insured through an auto policy. We provide complete documentation for both — HIN certificate, NMMA certification, VIN plate, and LSV compliance label — making the paperwork straightforward for any knowledgeable broker. We also have brokers that can assist with this.

Check the Watercar buying process and reserve your Watercar Now.

Your $5,000 deposit reserves a build slot for the WaterCar EV and is credited toward your purchase price. Build slots are allocated in the order deposits are received.

Your deposit is refundable.

To pay by wire transfer, email info@watercar.com for instructions, which are verified by phone with our Business Manager.

Prefer to pay by wire? Request wire instructions

This Watercar, Inc. Deposit Agreement (the “Deposit Agreement”) governs the placing of a reservation and making a deposit with Watercar, Inc. for a test drive and potential purchase of a Watercar EV Vessel (the “Watercar EV Vessel”). Please read all of these terms and conditions carefully before signing this Deposit Agreement and submitting your deposit. This is a binding agreement between you (the “Buyer”) and Watercar, Inc.

This Deposit Agreement outlines the reservation and deposit terms for a Watercar EV Vessel. Your reservation becomes effective only once you have paid the deposit amount listed below to Watercar, Inc., and the order of delivery will be determined on a first-deposit, first-delivery basis. This Deposit Agreement is subject to the following terms:

Model: Watercar EV*

Deposit Amount: $5,000.00

Deposit Refundable: The Deposit Amount is refundable up until a Purchase Agreement is entered into between Buyer and Watercar, Inc. for the ultimate purchase of a Watercar EV Vessel.

Transferable: This Deposit Agreement can be assigned by you to another purchaser upon the written consent of Watercar, Inc. and is subject to the terms and conditions of this Deposit Agreement.

* The Watercar EV Vessel details and specifications may vary from your Watercar EV Vessel and are subject to change without notice, and will be confirmed prior to start of production.

Now, therefore, in consideration of the mutual covenants set forth herein and other good and valuable consideration, Watercar, Inc. and Buyer agree as follows:

1. DEPOSIT. By entering into the Deposit Agreement, Buyer agrees to pay Watercar, Inc. the Deposit Amount set forth above for the placing of a reservation and a test drive of one Watercar EV Vessel. By agreeing to these terms and conditions, you represent and warrant to Watercar, Inc. that you are at least 18 years of age. If you are reserving a Watercar EV Vessel on behalf of a company, organization, or entity (the “Entity”), you represent and warrant that you have the authority to bind that Entity to this Agreement and that such Entity agrees to be bound by this Deposit Agreement.

2. TEST DRIVE. To schedule a test drive of a Watercar EV Vessel, Watercar, Inc. requires any Buyer or perspective buyer to make a deposit payment pursuant to the terms of this Agreement and execute a separate agreement entitled Boat Test Drive Liability Release and Hold Harmless Agreement. This policy is in place to confirm the commitment of prospective buyers and to cover any potential damage during the test drive, as such deposit may be subject to forfeiture if such damages are caused by the Buyer’s conduct or negligence during the test drive.

3. DELIVERY NUMBER. Upon receipt of a signed Deposit Agreement and payment of the Deposit Amount, Watercar, Inc. will assign buyer a delivery number (the “Delivery Number”). Delivery Numbers are assigned on a first-deposit, first-produced basis and are subject to prior commitment and availability as determined by Watercar, Inc. at its sole discretion. There is no guarantee as to a delivery date based on your Delivery Number, and delivery timing is subject to Watercar, Inc.’s manufacturing schedule, delivery and service operations, and ultimate execution of a Purchase Agreement.

4. DEPOSIT SHALL BE APPLIED TO PURCHASE. The $5,000 deposit made by Buyer to Watercar, Inc. and transmitted to Watercar, Inc. upon execution of this Deposit Agreement shall be deducted from the Purchase Price provided Buyer completes the purchase of the reserved Watercar EV Vessel.

5. TERMINATION

5.1 Buyer may cancel this Deposit Agreement by providing written notice to Watercar, Inc. any time prior to execution of a Purchase Agreement. In the event that the Buyer timely cancels the Deposit Agreement, Watercar, Inc. will return the deposit to the Buyer, minus any credit card, bank , or other processing fees, within ten (10) business days, subject to any possible forfeiture pursuant to Section 2 above.

5.2 Watercar, Inc. may terminate this Deposit Agreement for cause upon written notice to Buyer if Buyer fails to comply with this Deposit Agreement.

6. LIMITATION OF LIABILITY

NOTWITHSTANDING ANYTHING TO THE CONTRARY, THE MAXIMUM LIABILITY OF WATERCAR, INC.’S OR ANY OF ITS AFFILIATES’, OR THEIR RESPECTIVE OFFICERS’, EMPLOYEES’, LICENSORS’, AND PARTNERS’ AGGREGATE LIABILITY TO BUYER FOR ANY BREACH OF THIS DEPOSIT AGREEMENT SHALL BE A FULL REFUND OF THE DEPOSIT MADE BY BUYER. IN NO EVENT SHALL WATERCAR, INC. BE LIABLE FOR ANY CONSEQUENTIAL, INDIRECT, PUNITIVE, INCIDENTAL OR SPECIAL DAMAGES ARISING OUT OF OR RELATING TO THIS DEPOSIT AGREEMENT.

7. GOVERNING LAW

This Deposit Agreement shall be governed by the laws of the State of California. Any and all disputes between the Parties shall be resolved in the courts of Orange County, California or the United States District Court for the Southern District of California, to the exclusion of courts in any other country, state, county, or city.

8. PAYMENT SCHEDULE

Initial Refundable Deposit – $5,000 Due within five (5) business days of execution of Deposit Agreement.

First Payment – 40%: Due within five (5) business days of execution of Purchase Agreement.

Second Payment – 40%: Due at Mid-Build Milestone (per Milestone Notice), within five (5) business days of notice from Seller.

Final Payment – 20%: Due no later than five (5) business days prior to delivery, and in any event prior to transfer of title.

All payments must be made by bank wire transfer. Buyer shall verify wire instructions by telephone with Seller’s Business Manager before initiating any transfer. Seller will never issue revised or updated wire instructions by email. Seller is not responsible for funds misdirected due to Buyer’s failure to verify instructions or reliance on altered/fraudulent communications.

(required)

"*" indicates required fields